As famous in our 2025 National Housing Forecast, at a nationwide degree, we count on that housing stock will proceed to enhance as steadily dropping mortgage charges and time assist to ease the lock-in impact on current owners and builders proceed to ramp up manufacturing, constructing properties to fill the big housing deficit. While nationwide house gross sales are anticipated to edge simply barely greater amid moderating house value development, some markets throughout the nation are projected to see a lot stronger development in each gross sales and costs in 2025. Across these markets, we discover various unifying themes:

- Regional focus within the South and West;

- Considerable latest gross sales development and probability of sustaining that momentum;

- More plentiful stock, in lots of circumstances pushed by new development;

- Younger populations, lots of whom are linked to the navy or have worldwide ties;

- Factors that reduce the impression of excessive mortgage charges, reminiscent of greater shares of outright homeownership (no mortgage debt) and populations eligible for government-backed mortgage loans like Veterans Affairs (VA) and Federal Housing Administration (FHA) loans; and

- Relatively lower-cost markets that proceed to profit from versatile work preparations.

The Sun Belt stays on prime

The prime 10 markets for 2025 are completely within the South and West, with a number of markets from three states—Texas (No. 4 El Paso and No. 7 McAllen), Florida (No. 2 Miami and No. 6 Orlando), and Virginia (No. 3 Virginia Beach and No. 5 Richmond)—rising to the highest of the checklist. Other states with markets within the prime 10 embody Colorado (No. 1 Colorado Springs), Arizona (No. 8 Phoenix), Georgia (No. 9 Atlanta), and North Carolina (No. 10 Greensboro).

We ranked the 100 largest metros by their summed anticipated sale and value development charges. These are the highest 10 metropolitan areas that surfaced for 2025:

Why are these markets within the prime 10? From a technical standpoint, they make the checklist as a result of we forecast these markets to be the leaders in house gross sales and value development in 2025 throughout the 100 largest markets.

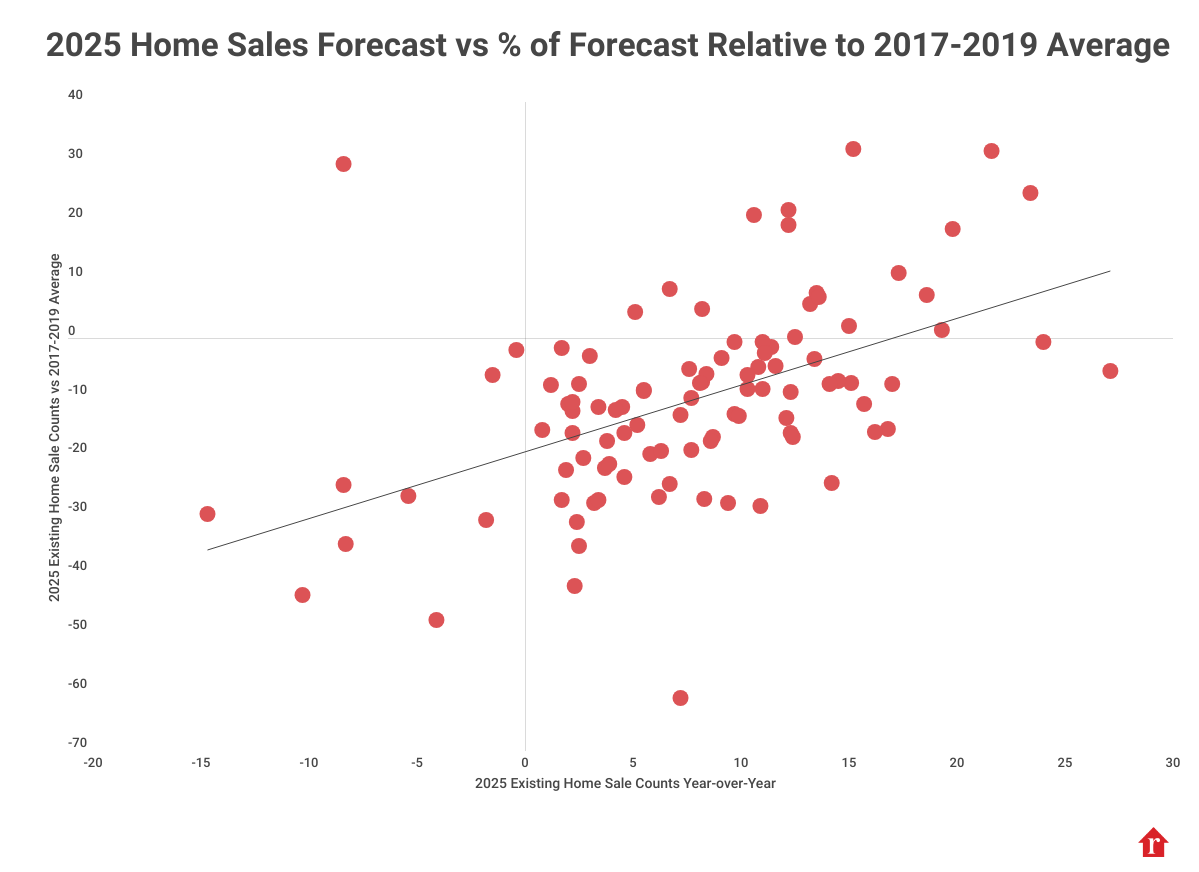

Going past the technicalities, nonetheless, reveals us a correlation between the 2025 proportion enhance in house gross sales throughout these markets and the 2025 house gross sales forecast relative to a market’s 2017–19 house gross sales common.

In less complicated phrases, the markets we’re forecasting to guide the nation in house gross sales in 2025 are markets which have higher recovered to their pre-COVID-19 ranges of house gross sales, and we count on them to carry that momentum within the yr forward.

We’ve dug even deeper into what separates our prime markets from the remainder of the pack—and have surfaced a number of key findings. Not solely are these more-recovered gross sales markets with a capability to develop on that momentum, however they’re additionally areas the place the supply of housing stock creates alternative. Although affordability remains to be stretched for a lot of households in these markets, as is the case nearly all over the place, aspiring owners can create alternatives and entry homeownership because of government-backed mortgage applications that allow decrease down funds. These applications are significantly worthwhile to the youthful households with navy and worldwide connections that decision these prime markets house.

Buyers have choices–each new and current properties on the market

Nationwide, the restoration of housing stock is nicely underway, with the variety of properties on the market in November notching the best mark since December 2019. Still, this stays a glass half-empty or half-full story. Despite the numerous positive factors up to now, nationwide, the housing market nonetheless trails the 2017 to 2019 common for November by 20%. Further, as we’ve identified in our month-to-month Housing Trends report, there’s notable regional variation within the stock restoration, with the South and West usually far nearer to pre-pandemic stock ranges than the Midwest and Northeast. This is undoubtedly an element propelling house gross sales development within the prime markets, half of which have lively itemizing counts above 2019 ranges in the latest information.

New development is a vital a part of the story. Eight of the highest 10 metros have seen year-over-year development by way of single-family house permits issued yr up to now. While many of those similar areas have seen declines in whole permits issued as multifamily constructing lags, single-family permits are what matter most for the owner-occupied housing market because the overwhelming majority of multifamily items will finally be leases whereas single-family properties are usually bought to owner-occupants. Nationally, new-construction listings make up 17.3% of the listings on Realtor.com®. All however two of the highest 10 markets (Miami and Phoenix) are close to this mark or higher.

Responding to the dearth of affordability within the housing market, homebuilders have just lately centered on smaller properties to satisfy demand. In half of the 2025 Top Housing Markets, new-construction costs have fallen previously yr, however in prime markets in Florida, Virginia, and North Carolina, new-construction house costs proceed to climb.

But new-home development is just not the one a part of the story. A restoration of existing-home sellers in these markets appears to be giving house customers quite a lot of selections that’s serving to to propel gross sales. In truth, regardless of the uptick in single-family house development in these prime markets, the share of new-construction house listings in 8 of the highest 10 markets has fallen as a restoration in existing-home sellers balances the uptick in new properties on the market.

Home to youthful households with navy and worldwide connections

Younger households are much more widespread in these prime 10 markets. All besides Miami have an above-average share of households below age 35. Further, most of those areas additionally over-index on prime-working-aged households, with above-average shares of households within the 35–54 vary, as nicely. Perhaps not surprisingly, households in these prime markets are additionally extra probably than the standard U.S. family to have kids.

On common, 28.8% of households in prime markets have kids, in contrast with 26.5% nationwide. McAllen (38.2%) drives up the common, however 7 of the highest 10 markets, together with Colorado Springs (27.8%), Virginia Beach (27.2%), El Paso (33.8%), Orlando (27.2%), Phoenix (27.7%), and Atlanta (29.3%), all have an above-average share of households with kids. Although the share of homebuyers with kids at house has declined, life modifications reminiscent of marriage, additions to the household, kids shifting out, and retirement proceed to be a prime purpose households say that they’d transfer.

Among the highest 10 metros, households usually tend to be linked to the navy. Among the 100 largest metros, roughly 1 in 8 households is an active-duty or veteran family, whereas among the many prime markets, the common is greater than 1 in 7.

In Colorado Springs (31.4%) and Virginia Beach (31.5%), the share of navy households is almost 1 in 3. They are adopted by El Paso (18.8%), Richmond (13.7%), and Phoenix (13.6%). This connection could have an effect on the housing market in two key methods. First, active-duty navy households have a tendency to maneuver extra typically, on common each two to a few years. Second, active-duty navy and veterans may be eligible for VA mortgage mortgage advantages, which play an necessary position in enabling homeownership.

Another widespread theme present in these markets is residents’ worldwide connection. On common, 17.6% of residents within the prime markets are foreign-born, starting from a low of 6.8% in Colorado Springs and Virginia Beach to a excessive of 42.7% in Miami. The share of foreign-born within the prime 10 markets is 4.6 proportion factors greater than the common share within the 100 largest markets. El Paso (22.5%), McAllen (25.8%), and Orlando (21.9%) additionally see a excessive share of foreign-born residents. Perhaps due to the worldwide connections of present residents, these areas additionally entice worldwide house customers. Notably, El Paso and McAllen acquired 6 occasions and 5 occasions the worldwide view share of a mean top-100 market, respectively. Meanwhile, Miami’s worldwide view share was 2.5 occasions that of the common top-100 market. Colorado Springs, Virginia Beach, and Phoenix additionally every recorded the next share of worldwide site visitors than the top-100 metro common within the yr ending in August 2024.

Outright possession insulates some markets from the drag of still-high mortgage charges

McAllen is certainly one of simply two of the 100 largest housing markets the place a majority of house owners (61.7%) personal their house with out a mortgage. Among the highest 10 markets, El Paso (49%), Miami (43.8%), and Greensboro (38.2%) are additionally areas the place an above-average share of households personal their house outright, with out a mortgage. Lower shares of house owners with mortgage debt signifies that the mortgage fee lock-in impact has much less bearing on homebuying and promoting selections in these areas within the mixture. Nationwide, our 2025 Housing Forecast anticipates that the mortgage fee lock-in impact will ease in 2025, however nonetheless be a limiting constraint for a lot of households.

While authorities mortgages create alternatives in different prime markets

However, within the remaining six markets, a bigger than common share of house owners carry a mortgage, with Virginia Beach (71%) and Colorado Springs (70.7%) main the best way.

Notably, government-backed lending, together with Veterans Affairs (VA) mortgages, Federal Housing Administration (FHA) mortgages, and United States Department of Agriculture (USDA) mortgages, is extra prevalent in markets anticipated to see prime gross sales and residential value development in 2025. More than half of mortgages had been authorities loans in Colorado Springs, El Paso, and Virginia Beach because of excessive VA mortgage utilization. Almost 3 in 4 mortgage loans had been authorities loans in El Paso, with 29.3% VA loans and 41% FHA loans.

One key benefit of government-backed mortgages is that they allow decrease down funds (within the case of VA and USDA loans, as little as 0%) whereas FHA loans usually require a minimal 3.5% down fee. Because government-backed mortgages are extra incessantly utilized in these markets, the common down fee as a share of house value is decrease than the nationwide common (14.3%), and in three markets—Virginia Beach, El Paso, and McAllen—the mix of decrease down fee shares and lower-priced properties signifies that the standard latest down fee was lower than $10,000.

Flexible work advantages comparatively lower-cost markets

Flexible work preparations, together with hybrid and absolutely distant choices, proceed to be interesting to homebuyers who will see solely a modest enchancment in general affordability in 2025. A earlier research by Realtor.com revealed that many house customers leverage versatile work modes to handle affordability challenges, and we count on that development to proceed.

According to WFH Data, half of the highest markets, together with Richmond (11.8%), Atlanta (10.8%), Phoenix (10.6%), Colorado Springs (8.9%), and Orlando (8.8%), have the next share of absolutely distant or hybrid on-line job postings in 2024 in contrast with the common share throughout the highest 100 metros (8.6%). While markets like Virginia Beach (7.8%) and Greensboro (6.1%) have a decrease share of distant or hybrid job postings, these areas have a value benefit over close by metros reminiscent of Washington, DC (17.8%), Raleigh (13.4%), and Charlotte (9.1%) that supply extra plentiful versatile job alternatives. The mixture of relative affordability and reasonable proximity for an occasional commute is more likely to profit these prime housing markets.

While the highest markets on common have a cheaper price level than the top-100 market common or the U.S. median, they’re present in areas with comparatively decrease incomes. As a end result, regardless of their decrease prices, the standard share of earnings required to afford a house within the prime markets is predicted to be 31.1%, barely greater than the nationwide common of 29.2%. Miami is on the excessive finish of the vary, at 42.1%, whereas Greensboro is on the low finish, at 25%.

Although housing affordability is just not higher than common, the highest markets do provide a considerably decrease value of dwelling than the nationwide common. The most inexpensive market is McAllen, the place the standard value of requirements is about 13% under the nationwide common, in accordance with a Realtor.com evaluation of regional value parities (RPPs) information from the Bureau of Economic Analysis. On the opposite finish of the spectrum is Miami, the place the price of dwelling is about 11.5% greater than the nationwide common. Overall, 7 of the highest 10 markets are extra inexpensive than the U.S. by way of value of dwelling.

Realtor.com® 2025 Housing Forecast–100 Largest U.S. Metros (Ranked)

| Rank | Cbsa Title | 2025 Existing Home Sale Counts Year-over-Year | 2025 Existing Home Sale Counts vs 2017–19 Average | 2025 Existing Home Median Sale Price Year-over-Year | 2025 Existing Home Median Sale Price vs 2017–19 Average | Combined 2025 Existing Home Sales and Price Growth |

| 1 | Colorado Springs, Colo. | 27.1% | -5.6% | 12.7% | 88.9% | 39.8% |

| 2 | Miami-Fort Lauderdale-West Palm Beach, Fla. | 24.0% | -0.7% | 9.0% | 100.5% | 33.0% |

| 3 | Virginia Beach-Norfolk-Newport News, Va.-N.C. | 23.4% | 24.5% | 6.6% | 57.3% | 29.9% |

| 4 | El Paso, Texas | 19.3% | 1.3% | 8.4% | 71.1% | 27.8% |

| 5 | Richmond, Va. | 21.6% | 31.7% | 6.1% | 68.8% | 27.6% |

| 6 | Orlando-Kissimmee-Sanford, Fla. | 15.2% | 32.1% | 12.1% | 82.6% | 27.3% |

| 7 | McAllen-Edinburg-Mission, Texas | 19.8% | 18.4% | 7.0% | 47.5% | 26.8% |

| 8 | Phoenix-Mesa-Scottsdale, Ariz. | 12.2% | 19.1% | 13.2% | 76.1% | 25.5% |

| 9 | Atlanta-Sandy Springs-Roswell, Ga. | 15.1% | -7.7% | 10.2% | 51.9% | 25.3% |

| 10 | Greensboro-High Point, N.C. | 17.3% | 11.0% | 7.7% | 51.6% | 25.0% |

| 11 | Tucson, Ariz. | 12.5% | 0.1% | 12.4% | 40.3% | 24.8% |

| 12 | Austin-Round Rock, Texas | 14.5% | -7.4% | 10.2% | 89.1% | 24.7% |

| 13 | Durham-Chapel Hill, N.C. | 14.1% | -7.8% | 10.1% | 102.0% | 24.2% |

| 14 | Charlotte-Concord-Gastonia, N.C.-S.C. | 15.7% | -11.2% | 8.4% | 92.6% | 24.1% |

| 15 | Little Rock-North Little Rock-Conway, Ark. | 18.6% | 7.3% | 4.8% | 49.6% | 23.4% |

| 16 | Jacksonville, Fla. | 13.5% | 7.6% | 9.8% | 69.6% | 23.3% |

| 17 | Cape Coral-Fort Myers, Fla. | 13.2% | 5.7% | 9.6% | 64.2% | 22.8% |

| 18 | Washington-Arlington-Alexandria, DC-Va.-Md.-W. Va. | 17.0% | -7.9% | 5.0% | 94.1% | 22.0% |

| 19 | Harrisburg-Carlisle, Pa. | 16.8% | -15.5% | 5.1% | 64.3% | 21.9% |

| 20 | Denver-Aurora-Lakewood, Colo. | 13.6% | 6.9% | 8.0% | 89.3% | 21.6% |

| 21 | Lakeland-Winter Haven, Fla. | 10.6% | 20.8% | 10.3% | 32.6% | 20.9% |

| 22 | Tampa-St. Petersburg-Clearwater, Fla. | 9.1% | -3.4% | 11.8% | 98.7% | 20.9% |

| 23 | Allentown-Bethlehem-Easton, Pa.-N.J. | 12.3% | -16.2% | 8.0% | 97.7% | 20.4% |

| 24 | Columbia, S.C. | 12.1% | -13.7% | 8.2% | 47.1% | 20.3% |

| 25 | Riverside-San Bernardino-Ontario, Calif. | 11.4% | -1.6% | 8.8% | 82.5% | 20.2% |

| 26 | Urban Honolulu, Hawaii | 13.4% | -3.7% | 6.7% | 63.7% | 20.1% |

| 27 | Augusta-Richmond County, Ga.-S.C. | 14.2% | -24.7% | 5.8% | 115.2% | 20.0% |

| 28 | San Antonio-New Braunfels, Texas | 10.9% | -28.5% | 9.1% | 80.7% | 20.0% |

| 29 | Akron, Ohio | 15.0% | 1.9% | 4.2% | 76.5% | 19.2% |

| 30 | Seattle-Tacoma-Bellevue, Wash. | 12.2% | 21.7% | 6.9% | 72.1% | 19.0% |

| 31 | Baltimore-Columbia-Towson, Md. | 16.2% | -16.0% | 2.7% | 78.8% | 18.9% |

| 32 | Memphis, Tenn.-Miss.-Ark. | 8.3% | -27.4% | 10.5% | 52.5% | 18.8% |

| 33 | Deltona-Daytona Beach-Ormond Beach, Fla. | 7.2% | -61.2% | 11.5% | 65.7% | 18.7% |

| 34 | Philadelphia-Camden-Wilmington, Pa.-N.J.-Del.-Md. | 12.3% | -9.2% | 6.1% | 70.4% | 18.3% |

| 35 | Buffalo-Cheektowaga-Niagara Falls, N.Y. | 9.7% | -0.7% | 8.5% | 60.3% | 18.2% |

| 36 | Springfield, Mass. | 11.0% | -0.8% | 6.8% | 47.2% | 17.8% |

| 37 | Portland-Vancouver-Hillsboro, Ore.-Wash. | 11.1% | -2.6% | 6.7% | 100.4% | 17.8% |

| 38 | Las Vegas-Henderson-Paradise, Nev. | 5.5% | -8.9% | 12.3% | 59.9% | 17.8% |

| 39 | Toledo, Ohio | 10.8% | -5.0% | 6.7% | 51.2% | 17.5% |

| 40 | Scranton–Wilkes-Barre–Hazleton, Pa. | 11.6% | -4.8% | 5.7% | 62.5% | 17.4% |

| 41 | Albany-Schenectady-Troy, N.Y. | 10.3% | -6.4% | 6.6% | 41.8% | 17.0% |

| 42 | Winston-Salem, N.C. | 7.7% | -10.3% | 9.2% | 76.3% | 16.9% |

| 43 | New York-Newark-Jersey City, N.Y.-N.J.-Pa. | 11.0% | -8.7% | 5.9% | 55.8% | 16.9% |

| 44 | Chicago-Naperville-Elgin, Ill.-Ind.-Wis. | 12.4% | -16.9% | 4.5% | 114.7% | 16.8% |

| 45 | St. Louis, Mo.-Ill. | 9.7% | -13.0% | 7.1% | 76.5% | 16.8% |

| 46 | Dallas-Fort Worth-Arlington, Texas | 7.6% | -5.3% | 9.2% | 53.0% | 16.7% |

| 47 | Salt Lake City, Utah | 6.7% | 8.2% | 10.0% | 56.6% | 16.7% |

| 48 | Oxnard-Thousand Oaks-Ventura, Calif. | 8.2% | -7.5% | 8.0% | 54.4% | 16.3% |

| 49 | Stockton-Lodi, Calif. | 6.2% | -27.1% | 9.8% | 59.7% | 16.1% |

| 50 | Bakersfield, Calif. | 9.9% | -13.3% | 6.0% | 78.1% | 15.9% |

| 51 | Indianapolis-Carmel-Anderson, Ind. | 7.7% | -19.1% | 8.2% | 71.3% | 15.9% |

| 52 | Rochester, N.Y. | 8.7% | -16.8% | 6.8% | 93.6% | 15.5% |

| 53 | Cincinnati, Ohio-Ky.-Ind. | 8.2% | 4.8% | 7.3% | 84.8% | 15.4% |

| 54 | Lansing-East Lansing, Mich | 10.3% | -8.7% | 4.9% | 65.4% | 15.2% |

| 55 | Oklahoma City, Okla. | 8.4% | -6.1% | 6.6% | 57.8% | 15.0% |

| 56 | Houston-The Woodlands-Sugar Land, Texas | 7.2% | -13.1% | 7.3% | 101.9% | 14.5% |

| 57 | Cleveland-Elyria, Ohio | 9.4% | -28.1% | 5.0% | 82.5% | 14.4% |

| 58 | Boise City, Idaho | 2.0% | -11.2% | 12.3% | 58.1% | 14.4% |

| 59 | Milwaukee-Waukesha-West Allis, Wis. | 8.6% | -17.6% | 5.7% | 51.7% | 14.3% |

| 60 | Sacramento–Roseville–Arden-Arcade, Calif. | 5.2% | -14.8% | 8.9% | 77.3% | 14.1% |

| 61 | Greenville-Anderson-Mauldin, S.C. | 5.1% | 4.3% | 8.9% | 97.8% | 14.1% |

| 62 | Ogden-Clearfield, Utah | 2.2% | -12.5% | 11.8% | 34.1% | 14.0% |

| 63 | Kansas City, Mo.-Kan. | 6.7% | -24.9% | 6.9% | 91.9% | 13.6% |

| 64 | North Port-Sarasota-Bradenton, Fla. | 3.2% | -28.1% | 10.4% | 63.7% | 13.5% |

| 65 | Fresno, Calif. | 8.1% | -7.7% | 5.1% | 90.7% | 13.2% |

| 66 | Charleston-North Charleston, S.C. | 5.8% | -19.7% | 7.0% | 46.2% | 12.8% |

| 67 | Nashville-Davidson–Murfreesboro–Franklin, Tenn. | 4.5% | -11.7% | 8.3% | 60.6% | 12.7% |

| 68 | Minneapolis-St. Paul-Bloomington, Minn.-Wis. | 6.3% | -19.3% | 6.2% | 90.3% | 12.5% |

| 69 | San Francisco-Oakland-Hayward, Calif. | 4.6% | -23.6% | 7.5% | 62.0% | 12.1% |

| 70 | Knoxville, Tenn. | 3.7% | -22.2% | 8.3% | 88.0% | 12.0% |

| 71 | Grand Rapids-Wyoming, Mich | 3.9% | -21.4% | 7.7% | 65.3% | 11.6% |

| 72 | Raleigh, N.C. | 2.2% | -11.0% | 9.0% | 114.9% | 11.2% |

| 73 | Louisville/Jefferson County, Ky.-Ind. | 4.6% | -16.2% | 6.1% | 70.5% | 10.7% |

| 74 | San Diego-Carlsbad, Calif. | 3.4% | -27.5% | 7.3% | 74.3% | 10.7% |

| 75 | Palm Bay-Melbourne-Titusville, Fla. | 0.8% | -15.7% | 9.6% | 102.7% | 10.4% |

| 76 | Los Angeles-Long Beach-Anaheim, Calif. | 4.2% | -12.3% | 5.5% | 54.3% | 9.7% |

| 77 | Hartford-West Hartford-East Hartford, Conn. | 3.8% | -17.5% | 5.6% | 55.3% | 9.4% |

| 78 | Wichita, Kan. | 3.0% | -3.2% | 6.2% | 63.9% | 9.2% |

| 79 | Worcester, Mass.-Conn. | 1.2% | -8.1% | 8.0% | 66.8% | 9.2% |

| 80 | Columbus, Ohio | 3.4% | -11.7% | 5.7% | 50.8% | 9.1% |

| 81 | Tulsa, Okla. | 2.5% | -7.9% | 6.5% | 60.5% | 9.0% |

| 82 | Detroit-Warren-Dearborn, Mich | 2.4% | -31.3% | 6.2% | 96.7% | 8.6% |

| 83 | Chattanooga, Tenn.-Ga. | 2.2% | -16.2% | 6.3% | 99.9% | 8.5% |

| 84 | Syracuse, N.Y. | 1.7% | -1.7% | 6.7% | 90.3% | 8.4% |

| 85 | Omaha-Council Bluffs, Neb.-Iowa | 2.5% | -35.4% | 5.8% | 96.1% | 8.3% |

| 86 | Spokane-Spokane Valley, Wash. | -0.4% | -2.1% | 8.7% | 49.3% | 8.2% |

| 87 | Baton Rouge, La. | 5.5% | -9.1% | 2.7% | 73.4% | 8.2% |

| 88 | Des Moines-West Des Moines, Iowa | 2.7% | -20.5% | 4.9% | 46.2% | 7.6% |

| 89 | New Orleans-Metairie, La. | 1.7% | -27.5% | 5.9% | 82.8% | 7.5% |

| 90 | Pittsburgh, Pa. | 1.9% | -22.5% | 4.7% | 92.9% | 6.6% |

| 91 | Dayton, Ohio | 2.3% | -42.2% | 4.3% | 103.1% | 6.6% |

| 92 | Portland-South Portland, Maine | -1.5% | -6.4% | 6.1% | 86.0% | 4.6% |

| 93 | Boston-Cambridge-Newton, Mass.-N.H. | -1.8% | -30.9% | 5.6% | 59.1% | 3.8% |

| 94 | New Haven-Milford, Conn. | -8.4% | 29.5% | 9.7% | 71.6% | 1.3% |

| 95 | Bridgeport-Stamford-Norwalk, Conn. | -5.4% | -26.8% | 4.9% | 57.9% | -0.5% |

| 96 | Madison, Wis. | -8.4% | -25.0% | 5.5% | 37.8% | -2.9% |

| 97 | Birmingham-Hoover, Ala. | -8.3% | -35.0% | 2.3% | 83.4% | -6.0% |

| 98 | San Jose-Sunnyvale-Santa Clara, Calif. | -10.3% | -43.7% | 4.0% | 66.7% | -6.3% |

| 99 | Providence-Warwick, R.I.-Mass. | -14.7% | -30.0% | 7.2% | 51.4% | -7.5% |

| 100 | Albuquerque, N.M. | -4.1% | -48.0% | -4.2% | 80.5% | -8.3% |

Methodology

The Realtor.com model-based forecast makes use of information on the housing market and general economic system to estimate 2025 values for these variables for the 100 largest U.S. metropolitan statistical areas by inhabitants dimension. These markets are then ranked by mixed forecasted development in house costs and gross sales. Results are calculated to a few decimal locations and ranked at this diploma of specificity; there have been no ties. For publication, outcomes are rounded to 1 decimal place, and this can lead to minor variations between the rounded and unrounded sums.

{kind=link}