It’s secure to say that inventory buyers are closing out 2024 in a slightly upbeat temper. The markets posted substantial positive factors, with the S&P 500 surging practically 27% year-to-date.

Pick one of the best shares and maximize your portfolio:

The assist for the present bullish pattern is evident. The prospect of rate of interest cuts, coupled with stronger-than-expected company earnings, is driving market confidence. Adding to the bullish outlook, final month’s election noticed former President Trump safe a non-consecutive second time period, fueling hopes for a pro-business, pro-growth financial coverage.

Looking forward, Oppenheimer’s chief funding strategist, John Stoltzfus, believes this rally is way from over.

“Traders and buyers of bullish persuasion (of which we’re half) level to fundamentals that counsel the present resilience of the economic system and the inventory market seem poised to proceed into subsequent yr… Based on plenty of elements together with present stateside financial coverage, the resilience in financial progress, enterprise exercise, the buyer, and job creation evidenced lately and the present yr, we provoke a worth goal for the S&P 500 by year-end 2025 of 7100,” Stoltzfus asserted.

With Stoltzfus’ goal in thoughts, we turned our consideration to 2 shares which have earned a spherical of applause from Oppenheimer. According to the agency’s analysts, each are on monitor for enormous positive factors, together with one that would soar by practically 580%.

After operating the tickers by TipRanks’ database, it’s clear the remainder of the Street is in settlement, with every incomes a ‘Strong Buy’ consensus score. Let’s take a more in-depth have a look at what’s driving this broad-based enthusiasm.

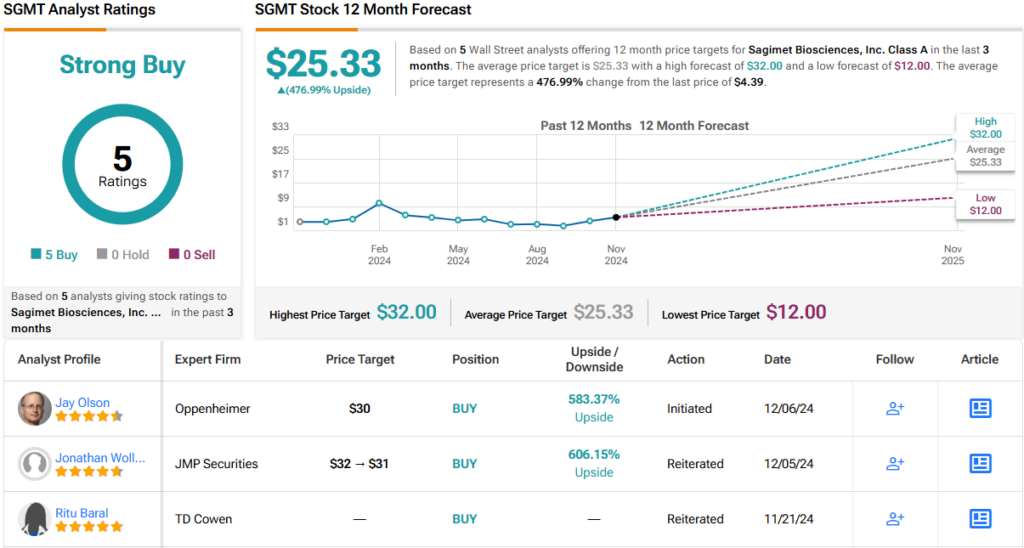

Sagimet Biosciences (SGMT)

We’ll begin with Sagimet Biosciences, the primary inventory to earn Oppenheimer’s backing – and for good motive. This biotech agency is pioneering a novel strategy to drug growth by its fatty acid synthase (FASN) inhibitors, a novel class of therapeutics with huge scientific potential.

Several illnesses are linked to the overproduction of the fatty acid palmitate, and Sagimet’s scientific pipeline goals to focus on the dysfunctional metabolic and fibrotic pathways related to these situations. Chief amongst them is metabolic dysfunction-associated steatohepatitis (MASH), a extreme liver dysfunction. As a key regulator of lipid synthesis, FASN represents a possible therapeutic goal for the therapy of this liver situation.

The FASN pathway is implicated in varied different situations, starting from comparatively widespread points like pimples to extra extreme illnesses comparable to most cancers. However, the MASH trial monitor stays the corporate’s most superior program.

On this entrance, Sagimet achieved a milestone earlier this yr by finishing the Phase 2b FASCINATE-2 trial. This examine evaluated denifanstat, the corporate’s flagship product, as a therapy for F2/F3 MASH — a stage the place sufferers expertise average to superior liver fibrosis. With no regarding security or tolerability points, denifanstat demonstrated a robust efficacy profile.

Sagimet is getting ready to launch a Phase 3 trial for denifanstat by the tip of the yr and is planning to increase the trial to incorporate sufferers with F4 MASH. The want for therapy on this space is immense, with round 22 million adults within the U.S. affected by MASH and restricted choices out there.

Beyond MASH, denifanstat can be being examined in China for pimples therapy, in collaboration with Ascletis. Acne affords one other vital alternative for Sagimet, because the FASN pathway performs a key position in sebum manufacturing, which contributes to the situation. The firm anticipates releasing topline outcomes from a Phase 3 trial within the second half of 2025.

Lastly, Sagimet is exploring denifanstat as a therapy for the aggressive mind most cancers glioblastoma, particularly recurrent glioblastoma multiforme (rGBM), together with bevacizumab. Phase 2 information of this mixture remedy met the first endpoint of progression-free survival (PFS), with a 31.4% six-month PFS in comparison with 16% for bevacizumab monotherapy. The Phase 3 trial, just like the pimples examine, is being carried out in China with Ascletis, with topline information anticipated within the first half of 2025.

Given denifanstat’s potential and SGMT’s $4.39 share worth, Oppenheimer analyst Jay Olson believes now’s the time to get in on the motion.

“SGMT’s present market cap is ~$141M, which to us seems undervalued primarily based on the promising MASH program with validation from massive pharma, e.g. NVO and LLY’s scientific efforts to increase incretin approval past weight problems into MASH and Boehringer Ingelheim’s latest $2B partnership with Suzhou Ribo Life Science Co. and Ribocure Pharmaceuticals to develop an siRNA-based MASH therapeutic… Our SOTP evaluation values denifanstat at $18/share in F2–F3 MASH, $2/share in F4 MASH, $1/share in recurrent glioblastoma, $5/share in moderate-to-severe pimples, and estimated money by YE24 at $4/share,” Olson acknowledged.

“While we see potential for denifanstat to draw market share by its differentiated efficacy and security as a monotherapy, its potential as a mixture remedy additional strengthens our conviction surrounding its industrial success if accepted,” the analyst added.

To this finish, Olson charges SGMT an Outperform (i.e. Buy), together with a $30 worth goal. Should the goal be met, a twelve-month acquire within the form of a considerable 583% might be in retailer. (To watch Olson’s monitor file, click on right here)

Turning now to the remainder of the Street, 5 Buys and no Holds or Sells have been revealed within the final three months. Therefore, SGMT boasts a Strong Buy consensus score. With the common worth goal standing at $25.33, the upside potential is available in at ~477%. (See SGMT inventory forecast)

Y-mAbs Therapeutics (YMAB)

The subsequent inventory we’ll have a look at is Y-mAbs, an oncology-focused biotech firm with one foot within the scientific trial stage and one within the commercialization stage. Y-mAbs’ accepted drug, DANYELZA, is a monoclonal antibody utilized in mixture with granulocyte-macrophage colony-stimulating issue (GM-CSF) to deal with pediatric sufferers aged 1 yr and older, in addition to adults, with relapsed or refractory high-risk neuroblastoma within the bone or bone marrow. It acquired FDA approval to be used within the US in November 2020.

While DANYELZA has contributed to Y-mAbs’ income stream and is increasing its geographic attain, the corporate’s SADA platform know-how has generated even better enthusiasm. This modern strategy makes use of a pre-targeted payload supply system, the place antibody constructs type tetramers that exactly bind to tumor targets. Y-mAbs sees this know-how as a transformative software in oncology, with the potential to focus on a wide selection of cancerous tumors with unmatched precision.

Y-mAbs is at present conducting early-stage human scientific trials on GD2-SADA, certainly one of its scientific merchandise related to this know-how. The Phase 1 trial targets strong tumors expressing GD2, comparable to SCLC, melanoma, and sarcomas, with drug administration scheduled at various intervals earlier than the usual 177Lu-DOTA therapy. Divided into three components, the trial is anticipated to ship Part A outcomes early subsequent yr. This preliminary part goals to determine the optimum protein dosage and set up the best timing between the administration of the SADA protein and its subsequent payload.

Another key scientific candidate from the SADA platform is CD38-SADA, which, because the identify suggests, targets CD38 — a protein discovered on the floor of sure blood most cancers cells. Y-mAbs is advancing a Phase 1 dose-escalation examine geared toward evaluating the protection, tolerability, and optimum dosing of CD38-SADA PRIT, a two-step remedy involving CD38-SADA and Lu177-DOTA, in adults with relapsed or refractory Non-Hodgkin Lymphoma.

Among the believers in Y-mAbs’ potential is Oppenheimer analyst Jeff Jones, who writes: “Our enthusiasm is centered on YMAB’s scientific stage SADA platform, as essentially the most superior pre-targeting platform at present in growth for supply of focused radiopharmaceutical therapies (TRT). The SADA platform has the potential to handle a crucial problem going through TRTs, off beam radiation publicity. YMAB’s number of targets for SADA might be key for his or her success, with particulars on future plans anticipated in early 2025. In addition to having two SADA primarily based candidates within the clinic by early 2025, YMAB is producing ~$90M yearly from DANYELZA gross sales in high-risk neuroblastoma (HRNB) which we view primarily as a strategy to offset SADA R&D funding.”

Backing his enthusiasm, Jones charges YMAB as an Outperform (i.e. Buy), and his $23 worth goal factors towards a one-year upside potential that approaches 144%. (To watch Jones’ monitor file, click on right here)

Overall, the inventory has picked up 5 analyst critiques – and people break right down to 4 Buys and 1 Hold, for a Strong Buy consensus score. At $31.20, the common worth goal is extra aggressive than Oppenheimer’s and implies ~231% upside potential. (See YMAB inventory forecast)

To discover good concepts for shares buying and selling at engaging valuations, go to TipRanks’ Best Stocks to Buy, a software that unites all of TipRanks’ fairness insights.

Disclaimer: The opinions expressed on this article are solely these of the featured analysts. The content material is meant for use for informational functions solely. It is essential to do your personal evaluation earlier than making any funding.

{kind=link}